Energy Update | November 4th, 2019

Are Natural Gas Fundamentals Supporting Higher Prices Long-Term? In my October 14th Energy Update, I said based on empirical evidence

Are Natural Gas Fundamentals Supporting Higher Prices Long-Term? In my October 14th Energy Update, I said based on empirical evidence

In my October 14th Energy Update, I said based on empirical evidence delineated in the report, I believed Natural Gas and Electricity prices were poised to increase long-term, and it was wise to secure energy agreements near the present price levels. I said in the near-term, weather factors could influence the direction of energy prices, but the downside reward potential of lower prices short-term was minimal versus the upside risk of higher prices long-term.

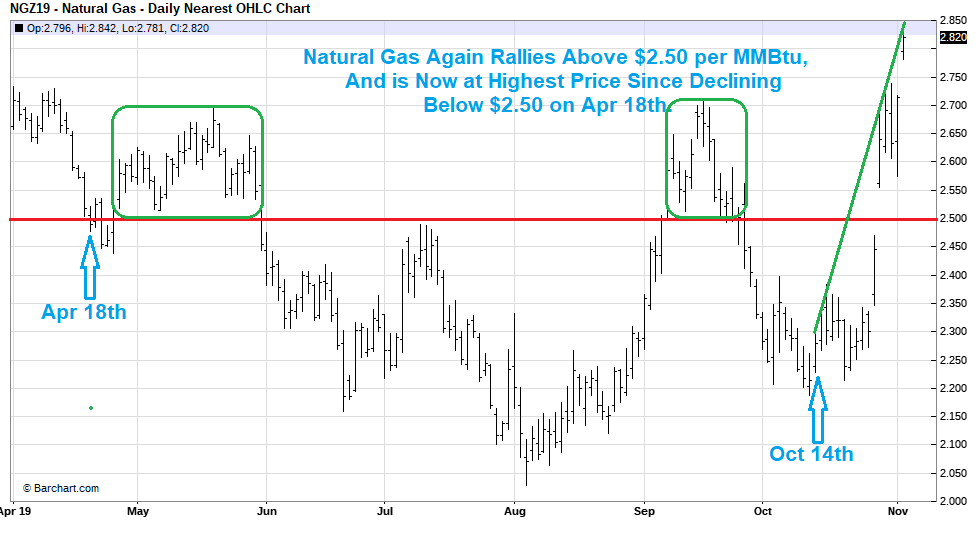

Since writing that report, Natural Gas sharply rallied 23% from $2.30 to $2.84 per MMBtu and is now at its highest price since declining below $2.50 per MMBtu for the first time since 2016 on April 18th.

As you can see in the above chart, after falling below $2.50 MMBtu on April 18th, Natural Gas briefly rallied above $2.50 twice before declining again below $2.50. The most recent rally was largely the result of cool weather throughout much of the United States increasing heating demand for Natural Gas short-term. But I believe a more important long-term factor is the production of Natural Gas is slowing. In my July 1st Energy Update, I explained based on fundamental factors, Natural Gas prices below $2.50 per MMBtu were offering hedgers a rare buying opportunity to lock in rates below where they would average longer-term.

The first factor discussed in my July 1st Energy Update, was the production of Natural Gas requires a large amount of ongoing capital investment (CAPEX). New wells must constantly be drilled to replace the huge volumes lost due to well depletions. When Natural Gas prices are high Exploration & Production companies have sufficient cash for the capital investment needed to drill new wells, but when prices are low, capital investment for new wells decline.

The question is; Is there evidence low Natural Gas prices are having an adverse effect on the ability of Exploration & Production companies to drill new wells, which will support higher Natural Gas prices long-term?

I believe the answer is absolutely yes.

Each week Baker Hughes has issued rotary rig counts as a service to the petroleum industry since 1944. In their last summary released Nov 1st, they reported the total count of active drilling rigs in the U.S. declined for the ninth time in 10 weeks, and over the last year, the total number of active Gas rigs declined 27.5% from 193 to 130 active rigs. This is an important development and explains why near-term shale production is declining as fewer new (and productive) wells are being drilled compared to last year.

But is there another factor supporting higher Natural Gas prices long-term?

Again, I believe the answer is, absolutely yes.

The second fundamental factor discussed on my July 1st Energy Update, was the demand for Natural Gas was expected to continue increasing due to increased exports of Liquified Natural Gas overseas, increased pipelines to Mexico and switching from Coal to Natural Gas for electric power generation. Since July 1st, the demand for Natural Gas continued increasing year over year, and if this trend continues into 2020, in conjunction with stagnant production, I believe Natural Gas prices will increase long-term.

One last point to consider.

If the present cooler than normal weather throughout much of the U.S. is followed by milder than normal weather, prices may again decline short-term. But if prices stay near or below $2.50 per MMBtu much longer, as I explained in my July 1st Energy Update, it will threaten the long-term survival of many E&P companies.

Low Natural Gas prices lead to the ominous combination of E&P companies decreasing CAPEX resulting in less production while increasing demand for exports and power for electric power generation. This combination will force many E&P companies to turn to debt for the capital needed to maintain production to keep up with increased demand and thereby increase their risk of bankruptcy.

Conclusions:

Long-term prices are primarily based on supply/demand factors, and as discussed in this report, I believe supply/demand factors support higher Natural Gas and Electricity prices long-term. In the near-term, weather factors will continue to influence the direction of energy prices, but the downside reward potential of lower prices short-term is minimal versus the upside risk of higher prices long-term.

Not every client’s risk tolerance and hedging strategy is the same, but the above report will help you put into perspective the risk/reward opportunities. I invite you to call one of our energy analysts to help you plan a hedging strategy appropriate for your situation.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit