Natural Gas’s Contango Market Predicting a Supply Deficit is Forthcoming in 2025?

Energy News Update: May 6 2024 Natural Gas’s Contango Market Predicting a Supply Deficit is Forthcoming in 2025? https://youtu.be/3DD9vGIVzbU Natural

Energy News Update: May 6 2024 Natural Gas’s Contango Market Predicting a Supply Deficit is Forthcoming in 2025? https://youtu.be/3DD9vGIVzbU Natural

Energy News Update: May 6 2024

![]() Natural Gasis the largest source of power for the generation of Electricity; therefore, their pricing is highly correlated, which is why we focus on Natural Gas in our reports.

Natural Gasis the largest source of power for the generation of Electricity; therefore, their pricing is highly correlated, which is why we focus on Natural Gas in our reports.

Our April 22nd Energy Update explained why Natural Gas becoming a Contango Market strongly suggested the average price will be higher long-term, and the upside risk is much greater than the downside potential of waiting and hoping for slightly lower prices.

The summary of forward market prices below clearly shows Natural Gas has become a Contango Market through 2027:

A market becomes a Contango market when its forward contract prices are higher than its nearby contracts, which is where Natural Gas is today with its forward market prices projected to average $2.72 per MMBtu for the remainder of 2024, $3.52 in 2025, $3.97 in 2026 and $4.05 in 2027.

Our Apr 22nd Energy Update explained Contango markets occur when traders believe short-term fundamentals supporting low prices are transitioning to long-term fundamentals supporting higher prices.

Fundamental analysis measures and predicts the factors affecting the future supply/demand of a commodity, and in this case, the factors impacting the future supplies of Natural Gas, which are predicting a supply deficit is forthcoming.

Today’s report summarizes the factors taking Natural Gas from its present supply surplus to a supply deficit in 2025.

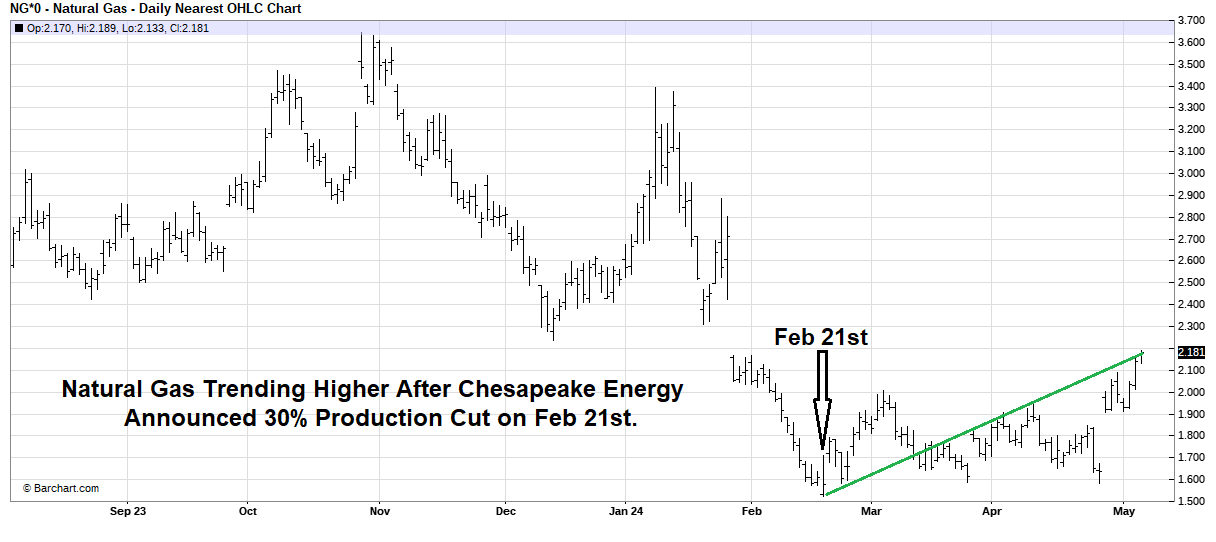

The first factor leading to a Natural Gas supply deficit next year was discussed In our Feb 26th Energy Update in which we said Natural Gas producers would be forced to cut production in response to today’s unsustainably low prices.

Simply put, prices are unsustainably low when they decline below the cost of production, and producers must respond by making strategic decisions to reduce production to force prices to move higher in the future.

This response was confirmed on Feb 21st when Chesapeake Energy in response to the recent plunge in prices, announced they were cutting the amount of fuel they will produce in 2024 by roughly 30%, and Natural Gas immediately reversed its decline from its lowest price of the year and has trended higher since their announcement.

The market’s response to this news was appropriate given Chesapeake Energy is expected to become America’s largest producer of Natural Gas after its merger with Southwest Energy, and was reinforced when EQT presently the largest U.S. Natural Gas producer, announced its strategic decision to cut production by approximately 1 Bcf per day starting in late February.

Baker Hughes’s latest report, released on May 3rd, confirmed that producers of Natural Gas are decreasing their production with active Gas rigs continuing to plunge now down 35% from this time last year going from 157 to 102 active rigs.

Therefore, the first factor expected to move Natural Gas from a supply surplus to a supply deficit is firmly in place, but another and even more powerful factor will likely force Natural Gas into supply deficits in 2025!

EXPORTS

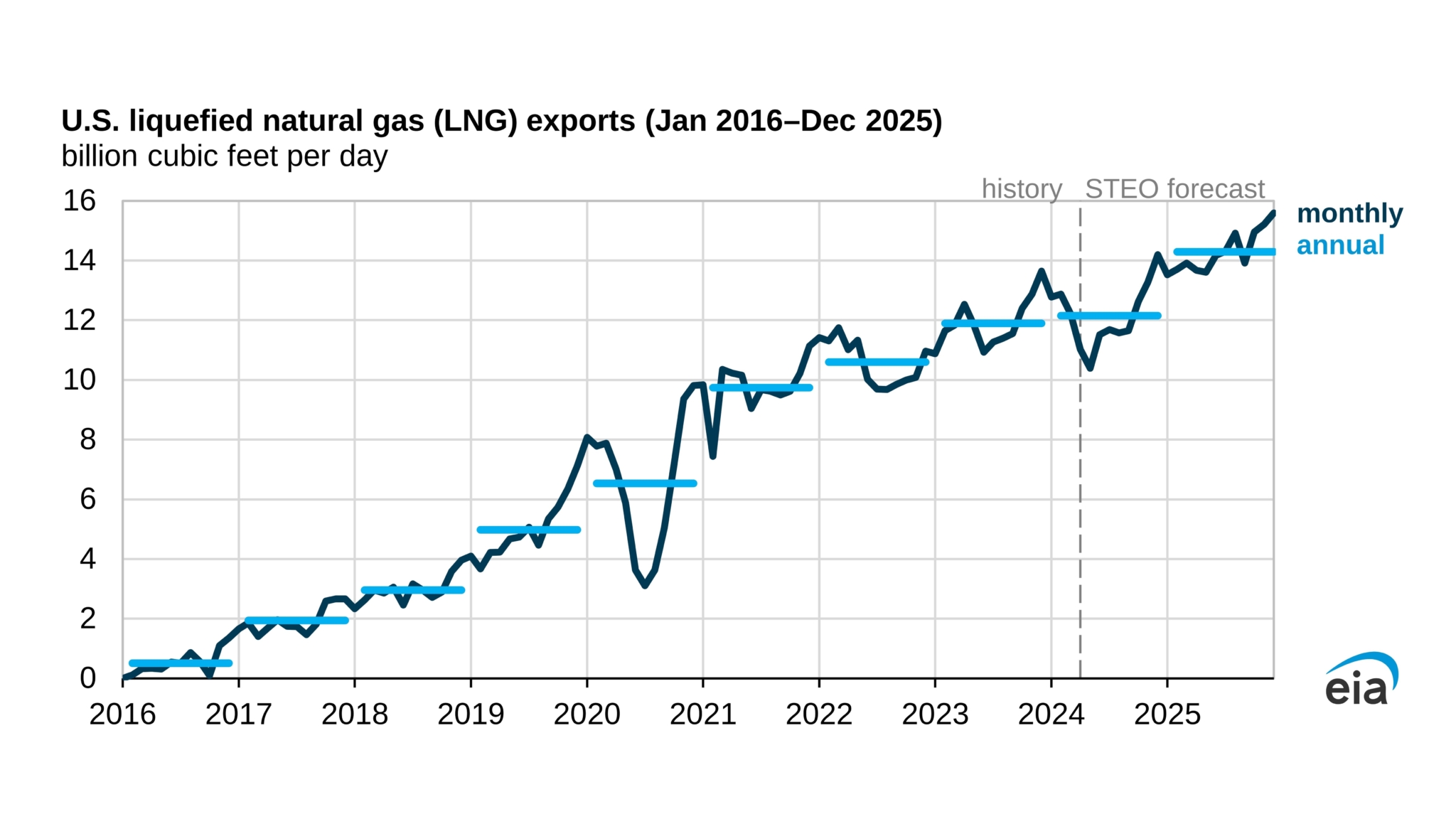

In their Apr 9th Short Term Energy Outlook (STEO), the Energy Information Administration (EIA) forecasted America’s liquefied Natural Gas (LNG) exports will continue their growth since 2016 with three LNG export projects presently under construction beginning operations and ramping up to full production by the end of 2025.

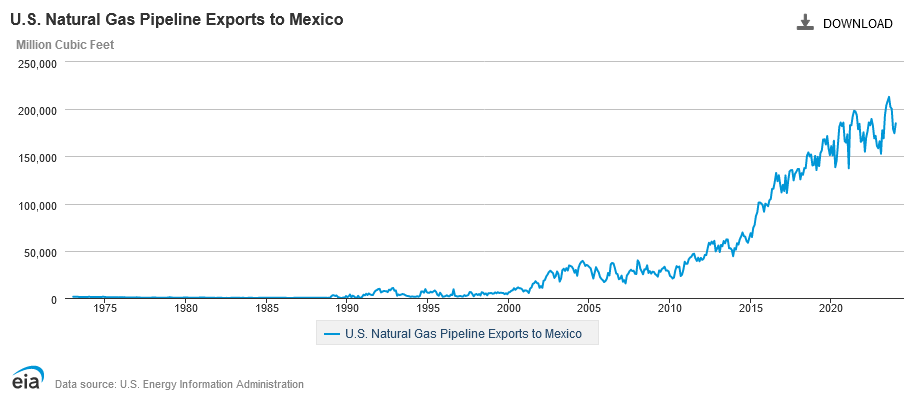

The EIA also forecasted another factor that will support the growth of America’s Natural Gas exports, our continued pipeline growth, mainly to Mexico:

In their STEO forecast, the EIA predicts America’s net exports of Natural Gas (exports minus imports) will grow 6% to 13.6 Bcf/d in 2024 compared to 12.8 Bcf/d in 2023, and in 2025, the EIA predicts net exports will increase an additional 20% going to 16.4 Bcf/d. If the EIA is correct and America’s net exports increase from 13.6 to 16.4 Bcf/d in 2025, the net result will be a 1,022 Bcf decrease in Natural Gas supplies in 2025.

In their latest May 2nd Weekly Natural Gas Storage Report, the EIA reported we presently have a 642 Bcf surplus in storage versus the 5-year average, which is why Natural Gas is presently near its lowest prices since 2000.

But based on the two factors discussed in today’s report, it is clear Natural Gas will be moving from supply surpluses in 2024 to supply deficits in 2025, and the Contango Market is predicting Natural Gas will respond with much higher prices in 2025 through 2027, but some of you may be tempted to delay because your local utility is presently posting low tariff rates with Natural Gas the largest source of power for the generation of electricity near a 20-year low.

Hopefully, today’s report will help anyone hesitating to secure a fixed rate with a supplier because their local utility is offering a low rate at this time, will understand those low rates will likely be much higher long-term.

A good lesson can be learned from what took place in Ohio last week. The Public Utilities Commission of Ohio (PUCO) encouraged Ohioans to review their energy choice options ahead of electricity supply price changes effective June 1, 2024.

What were those changes?

The tariff rates of the 6 local utilities will be decreasing from 14% to 32%, so why in the world is the PUCO encouraging Ohioans to review their energy choice options ahead of the decreases?

We believe it is because, since 2000, the PUCO knows when prices declined to where they are today, the average price was always much higher long-term.

Therefore, if your present energy agreement expires in 2024 or 2025, we recommend taking advantage of this year’s historically very low prices and reserving energy to be available when your present agreements expire.

We believe the empirical evidence in today’s report showing the forward market is now a Contango Market strongly suggests the average price will be higher long-term, and based on what has happened since 2000, we are likely still early in the present cyclical bull market and the longer you delay securing fixed rates now the more you will likely pay later!

Not every client’s risk tolerance and hedging strategy are the same, but hopefully, today’s report will help put into perspective your risk/reward opportunities. We invite you to call one of our energy analysts to help you plan a hedging strategy appropriate for your situation.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Don't have one? You can get one by calling us at 855-4-PKIOSK.

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

4.Local Company

5.Zone

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit