Energy Update | October 31st, 2018

Energy Update October 31st, 2018 Natural Gas Backwardation is Unsustainable and Will Likely Lead to Much Higher Prices in 2019

Energy Update October 31st, 2018 Natural Gas Backwardation is Unsustainable and Will Likely Lead to Much Higher Prices in 2019

Energy Update

October 31st, 2018

(My reports focus on Natural Gas as it is the largest energy source for the generation of Electricity; therefore, Natural Gas and Electricity are highly correlated.)

In my Oct 9th Energy update, I said the recent rally of Natural Gas was due to an already dire supply situation continuing to deteriorate with forecasts for colder than normal weather starting in mid-October causing supplies to fall further below the 5 Yr. Avg. by Oct 26th. But the good news was the market phenomenon called “Backwardation”, allowed hedgers to secure rates below present levels in the forward market.

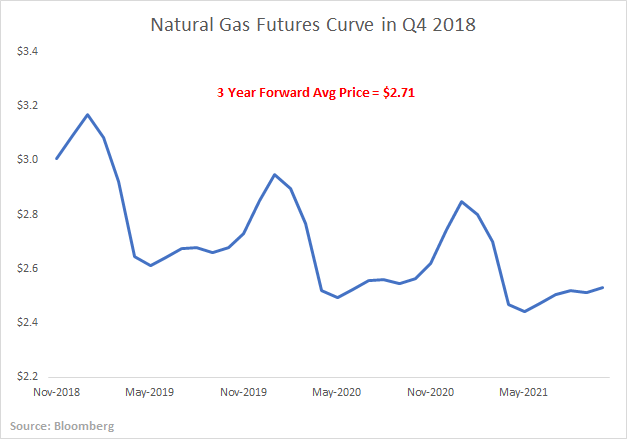

This was especially true when you considered the chart below:

Clearly when you can purchase a commodity near the lower end of its 20-year trading range while supplies are below the 5 Yr. Avg., it is prudent to do so, but this is especially true when a commodity such as Natural Gas has supplies starting its high demand winter heating season at the lowest level in 10 years.

In this report, I will explain why the Natural Gas Backwardation mentioned in my Oct 9th report is unsustainable and will likely lead to much higher prices in 2019 and beyond!

In my trading over the years I have learned commodity prices are primarily based on supply/demand fundamentals, but future estimates of supply/demand often contain false assumptions leading to inaccurate price estimates. The only explanation for the present Backwardation in Natural Gas prices is the market is assuming growth of supplies in future years will be enough to meet growth in demand. I believe this assumption is flawed for the following reasons:

It is important to note E&P companies are expected to report negative cash flow this year with the average price below $3 per MMbtu, and with the forward markets forecasting prices will remain below $3 per MMbtu over the next 3 years, E&P companies know they cannot generate profits if prices remain this low; therefore, they will likely reduce their production rates in 2019 to an annualized rate of 2% or less.

Therefore, based on the above factors, I believe we are at the precipice of major structural imbalances with increases in production not meeting increases in demand, and Natural Gas prices will likely head significantly higher in 2019 and beyond. The only factor that may delay prices moving higher in the near-term would be a mild winter, but this would only exacerbate the structural imbalances as production would remain muted with E&P companies reducing their capital expenditures due to negative cash flow.

Low prices are a disincentive for E&P companies to invest in drilling new rigs and motivates them to shut down operation of unprofitable rigs until pricing increases, and the longer prices stay low now, the longer the structural imbalances will remain in place and the higher prices will likely go later. Therefore, if your hedge contracts expire within the next 18-months, we strongly recommend reserving blocks of Natural Gas and Electricity to be available when your present contracts expire.

Conclusions:

Natural Gas Backwardation over the next 3 years is unsustainable because low prices are a disincentive for E&P companies to increase production, while increased demand caused by LNG projects coming on line more than doubling LNG capacity to 9 Bcf/d by the end of 2019, and the continued growth of Natural Gas exports to Mexico along with switching to Natural Gas from Coal for the generation of Electricity will result in structural imbalances likely leading to much higher prices in 2019 and beyond.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit