Warm Close to Fall Leads to Short-Term Natural Gas Decline, But Long-Term Risks Remain

Warm Close to Fall Leads to Short-Term Natural Gas Decline, But Long-Term Risks Remain In my November 22nd Energy Update,

Warm Close to Fall Leads to Short-Term Natural Gas Decline, But Long-Term Risks Remain In my November 22nd Energy Update,

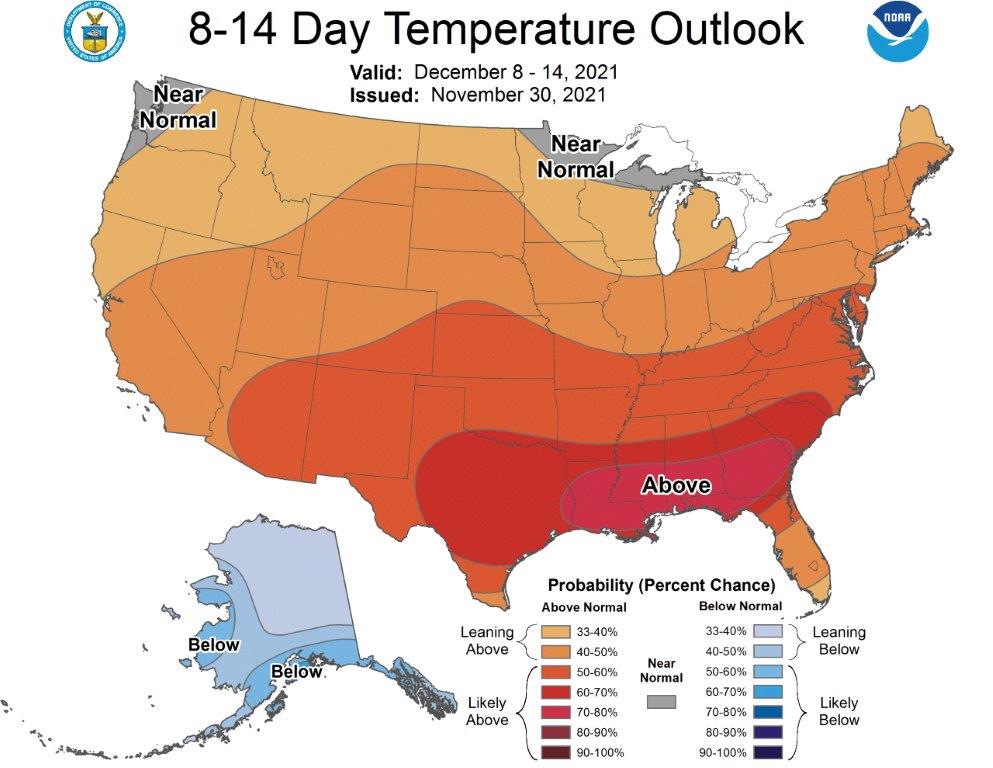

In my November 22nd Energy Update, I said Germany announced it suspended certification of a Russian gas pipeline called Nord Stream 2, which increased the risk of higher prices if we experienced a colder than normal winter. But since my last report, the weather forecasted for the first half of December in the United States has been much milder than expected:

In my Oct 11th, Energy Update, I said In my years of trading commodities, I have always focused on seasonal patterns to help determine my entry points, and there were four years similar to this year when Natural Gas rallied into the fall from lower prices; 2000, 2002, 2005 and 2013. And in each case, after Natural Gas pulled back in the fall it always rallied to a new high in December.

What is different this year? In those four examples, we did not end the fall with extraordinarily warm weather; therefore, the probability Natural Gas will rally to a new high this year in December is less likely given the unexpected warm weather in the first half of the month. But the decline in Natural Gas short-term does not materially change the risk of higher prices long-term.

The long-term risk factors remain. Since the beginning of the year, I warned energy prices were increasing due to the present administration’s restrictive energy policies, aggressive fiscal spending, and quantitative easing by the Fed were increasing the risk of inflation in the U.S.

And a 10-year low in Europe’s Natural Gas supplies caused by green energy policies increased the risk of higher prices not only this winter, but long-term since the polices leading to today’s high prices are not abating, they are becoming more entrenched here and abroad.

Therefore, I believe the short-term decline in Natural Gas is a long-term buying opportunity. Early in the 21st century, we experienced higher Natural Gas prices and extreme volatility prior to fracking giving us sufficient supplies to meet our energy needs, but over the last 10 years we have been blessed with a period of lower prices with fracking giving us enough supplies to meet our energy needs.

But the long-term risk factors discussed above has increased the potential we will return to the period of higher prices we experienced before fracking.

The warm end of this year’s fall season is not an accurate indication that we will experience a warm winter this year, several forecasters including the Farmers’ Almanac have predicted we will experience a colder than normal winter, and if we do, Natural Gas will likely reverse to a new high.

Hopefully today’s report has helped you understand why I believe the unexpected short-term decline in Natural Gas is an excellent opportunity for hedgers to protect themselves against the risk of higher Natural Gas and Electricity prices long-term.

Not every client’s risk tolerance and hedging strategy is the same, but the above report will help you put into perspective the risk/reward opportunities. I invite you to call one of our energy analysts to help you plan a hedging strategy appropriate for your situation.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Don't have one? You can get one by calling us at 855-4-PKIOSK.

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

4.Local Company

5.Zone

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit